High Earner Not Rich Yet: Multiple Six Figure Salary and Still Broke

This post may contain affiliate links. Click here to read my full disclosure.

Many would argue that six figures just isn’t enough anymore. If you’re a High Earner Not Rich Yet, or HENRY (for short), you might be wondering why? Maybe you’re living paycheck to paycheck, struggling to make ends meet or perhaps you’ve just overextended yourself.

It’s never too late to start making financial changes help you reach financial independence. A lot of the time, the reason people are broke is due to behavioral issues, but the good news is you are in charge of your own future!

It’s up to you to identify key behaviors and change the trajectory of your life. How do we do that? First, download the free cheat sheet of this post so you can get started setting your own financial goals (like saving money) so you can achieve the financial freedom you so desperately desire!

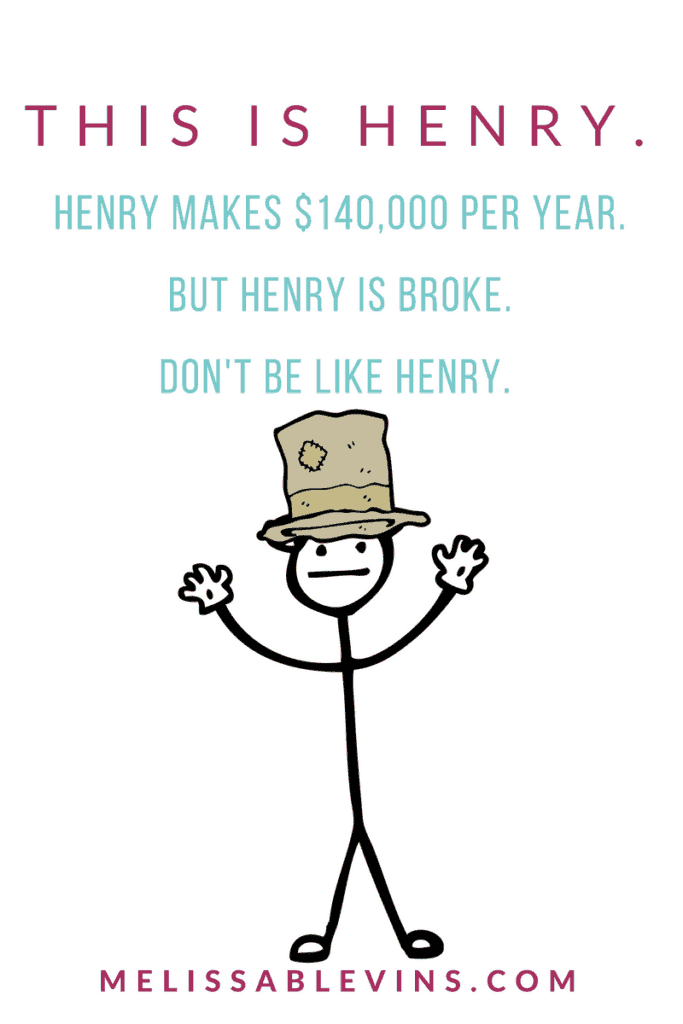

This is HENRY. Henry makes $140,000 per year. But Henry doesn’t feel like he makes that much. In fact, Henry feels weighed down by all of his financial responsibilities. While he makes a good income, he always seems to be broke…waiting for that next payday. Don’t be like Henry.

Side note: HENRY’s typically make $250k-$500k, but there’s no reason someone earning $100k plus can’t achieve financial freedom (plus it’s more realistic of a scenario).

So you earn a decent living but you’re still broke. How can you change that? Here’s the quickest and easiest way to see where you stand.

1. Create a Budget

You’ve got to see where your money is going if you’re going to change things. You’re not alone if you’ve been winging it and are afraid to write it all out. But I can promise you that you’ll feel better knowing your numbers (even if you’re not a geek like me).

Start by writing down your take-home pay (after taxes and all deductions).

Then list all obligations and expenses in order of importance (four walls first!). List your housing expenses including utilities and taxes first. Then list out your groceries, debts, and other expenses. As a HENRY (high earner not rich yet), you should have a good amount of income left after paying minimum payments on all debts and regular expenses. If not, it may be time to dig deeper into your account.

2. Check your Account

Next I want you to pull your bank statement. It’s okay if you have to log into online banking to do so, but I want you to print out your most recent transactions for 30 days. Now I want you to highlight each and every frivolous purchase or expense that was made in the last month.

- Did you spend a lot of money shopping?

- Did you eat out quite a bit?

- Is a large portion of your money going towards gifts for others?

Find out where your funds have been going and why you’ve been broke, and you’ll likely see a pattern that may shock you! My ex-husband (emphasis on the EX) used to spend $600+ every single month just on eating fast food! He wasn’t even eating steak meals. It was largely McDonald’s and Sonic. How in the hell is that even possible?!

This post contains affiliate links. If you click my link, I will earn a small commission (at no cost to you). It’s how the blog makes money, and I appreciate your support! You can find my full disclosure here.

3. Automate Savings

Once you’ve figured out where your money has been going, you can start to reallocate it for your future and things that truly matter to you.

Have you heard of the 50-20-30 rule of budgeting? 50% of your income goes towards household expenses, 20% goes towards savings, and 30% goes towards everything else (extras, fun, saving for a car, etc). You can apply this principal easily by setting up automatic transfers and deductions either from your employer or through online banking.

Whatever you do, make sure you automate the savings process, especially if you’re a free-spirited nerd like me. I struggle to manually make the transfers to savings (especially when I see something flashy I’d rather spend my money on).

If you’re looking for a great online savings account to put some money out of sight, out of mind, I highly recommend CIT Bank’s money market account.

The annual percentage yield is higher than that of most local community banks, and when the money is tucked away, it’s a bit more of a challenge to splurge in the moment.

I’m not saying you should put all of your money in an online account, but you can literally start an account with as little as $100 with no minimum balance requirements and no monthly fees, so no excuses! Start saving today!

It’s okay if you’re a high earner not rich yet! Take a deep breath and go through the steps. By creating a written budget every time you get paid, checking your account for discrepancies and crazy spending patterns, and automating your savings, you’re taking the first steps towards financial freedom! Remember that we are setting the example for future generations, and it’s up to us to take control of our finances and teach our kids how to manage their own money wisely! It all starts with you!